Banks that regularly improve customer experience (CX) grow 3.2x faster. According to PwC, 86% of customers are willing to pay more for better service, with 82% claiming they’re ready to share personal data in exchange for personalized experiences.

Good customer experience in banking builds trust, drives customer loyalty, and boosts growth through word of mouth, turning clients into ardent brand evangelists. It separates innovation-driven financial institutions from their slow-to-adapt competitors, helping them be one step ahead.

In today’s blog post, we’ll showcase the best CX practices that banks have been following to pull away from the pack. You’ll discover the top 5 banking customer experience trends shaping the industry in 2025 and beyond. Explore them and adapt them for your organization to deliver unmatched customer satisfaction.

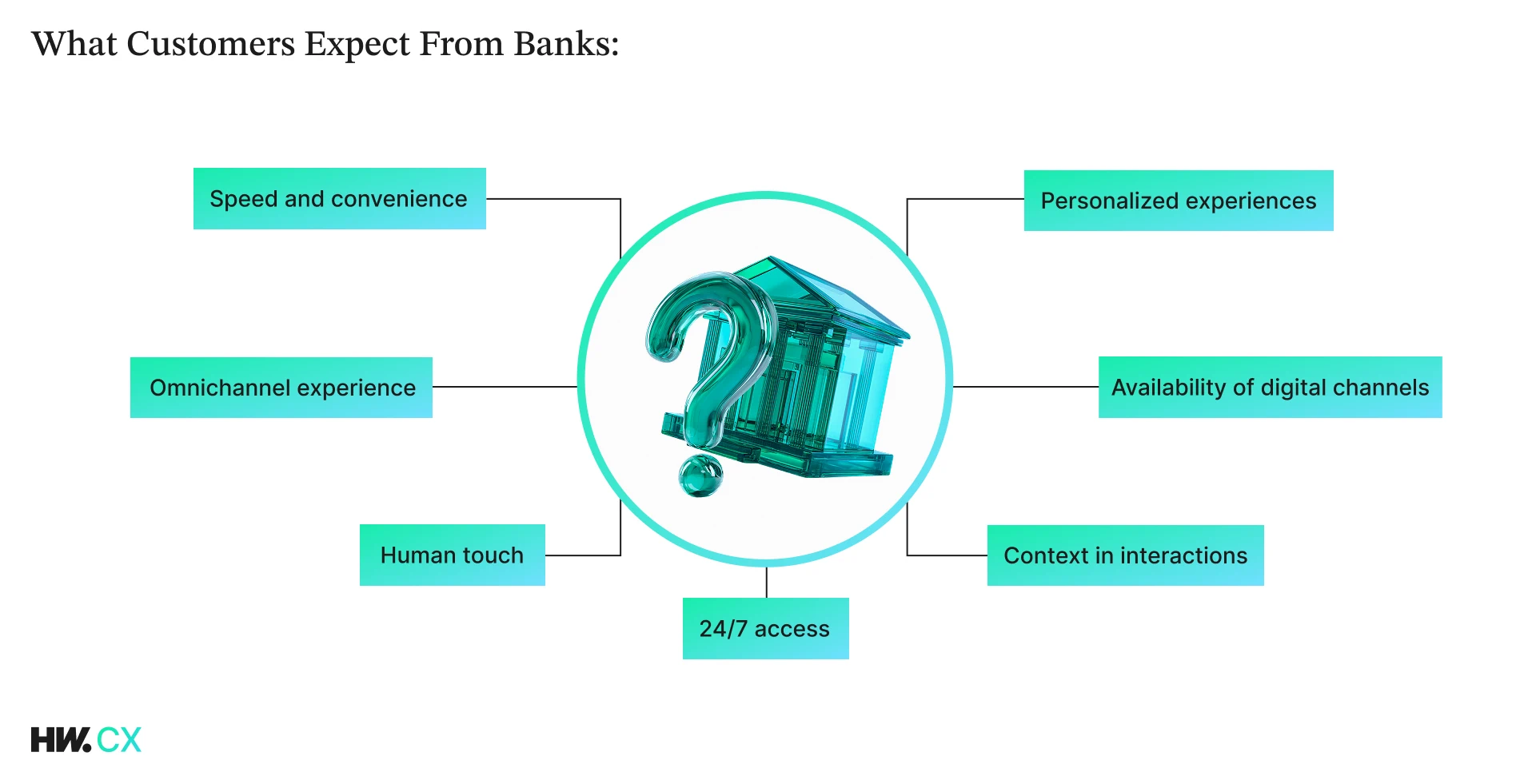

What Is Customer Experience in Banking? Customer Expectations from Banks

Customer experience in banking is about the feelings and perceptions a client has when interacting with a bank across its touchpoints. Whether using a mobile banking app, conversing with a customer support agent through email, or opening a bank account in a branch, every exchange matters and forms an enduring opinion about the service.

Importantly, when consumers engage with a bank, they’re not just comparing it to other banks; they’re measuring it against the best digital experience they’ve had recently. What’s more, 56% of consumers won’t even complain about bad service—they will silently switch to a competitor.

As the famous saying goes, “You never get a second chance to make a first impression,” so it’s critical to offer the smoothest user experience across every point of contact from the get-go. But how exactly can you do that? What do customers expect when interacting with your bank? After analyzing several reports, we can pinpoint these key customer expectations:

- Speed and convenience. 79% of consumers are willing to pay more for convenience and fast transactions (CX Network).

- Personalized experiences. 71% want personalized interactions. 76% experience frustration when personalization is lacking (McKinsey).

- Omnichannel experience. Over 62% of bank clients want smooth transitions between channels (from mobile and web to branch and vice versa). 40% report they won’t do business with a bank if it doesn’t provide their preferred communication channel (Zendesk).

- Context in interactions. 70% expect customer support agents to have complete context about their recent interactions with a bank for faster issue resolution (Zendesk).

- Availability of digital channels. 84% of customers rely on online banking and 72% use mobile banking apps frequently, indicating that digital channels are a must for organizations that care about customer engagement and satisfaction (CoinLaw).

- Human touch. Despite artificial intelligence (AI) gaining widespread adoption in the banking industry, many people, especially older generations, still appreciate human interactions. 25% of Gen Xers and Boomers regularly get in touch with human agents (Capgemini)

- 24/7 access. Customers believe that service availability is one of the staples of good customer experience in banking, with 89% demanding round-the-clock access to banking services (Zipdo).

Why Are Many Banks Slow to Innovate?

As you might expect, innovation is a prerequisite for a smooth digital banking customer experience. Yet, many banks are slow in that department. In fact, a 2020 Capgemini report revealed that banks in Europe and North America allocate up to 74% of their budgets to maintaining legacy systems, which naturally leaves very little room for innovation. You might be surprised, but 43% of banking systems are built on COBOL, with 80% of in-person transactions still using this outdated programming language. However, it’s not only the need for maintaining legacy systems that hinders digital transformation in banking organizations. Other factors also come into play.

Enter government regulations: As an industry dealing with finances and sensitive information, banking is heavily regulated. Banks must comply with anti-money-laundering (AML) rules, know-your-customer (KYC) regulations, General Data Protection Regulation (GDPR), capital requirements regulations, and many more standards, depending on the country and jurisdiction. To innovate and enhance customer service in banking, an organization must navigate the labyrinth of regulatory compliance frameworks, which, mind you, constantly change. This often turns the introduction of a new feature into a months-long (and budget-draining) venture.

Let’s also not rule out organizational inertia. The bigger a bank, the thicker its decision-making layer. Before an improvement decision reaches the production team, it must go through risk & compliance, management, accounting, and multiple other departments, which slows down the process and sometimes kills the initiative. Besides, bigger banks already earn significant profits from lending, deposits, and payments, so they are less incentivized to innovate and possibly cause disruptions to already well-functioning operations. However, fintechs and neobanks that provide the smoothest banking experience through innovative solutions start to challenge that dynamic.

In a nutshell, many banks are slow to innovate because innovation is time-consuming and requires significant investments that, let’s be honest, don’t always pay off. An extensive array of regulatory compliance requirements that a financial institution must adhere to whenever introducing a new product, service, or feature also contributes to the rigidity of the industry, making improvements hard to implement. Yet, despite all these challenges, many banking organizations still recognize the importance of good customer experience in banking and gradually find pathways to digital transformation.

Top 5 Banking Customer Experience Trends in 2025

Now let’s take a look at emerging consumer trends in banking and showcase organizations that have been using the latest technologies and tools to their benefit.

#1 Banking in your pocket, not in a branch

Modern consumers appreciate the convenience and time-saving benefits of mobile banking. The number of mobile banking users keeps growing and has reached 3.6 billion as of 2025. According to a recent survey, 77% of banking interactions now occur through digital channels, with 58% of millennials performing finance-related tasks on mobile apps daily. No wonder 95% of banks consider mobile banking their top investment priority in 2025.

It’s easy to see the appeal of mobile banking to users. It allows them to manage their finances without in-branch visits and long waits at the bank, which perfectly fits today’s busy lifestyles. It gives 24/7 access to accounts, enabling consumers to make transactions whenever they please, without having to wait for branches to open. It gives them a peace of mind and sense of control over their finances by providing insights into their spending and transaction history.

Naturally, it’s not only the users who benefit from mobile banking: Banks also get their share of the pie. First of all, mobile apps allow them to make their products and services accessible to a larger number of consumers and extend their customer base. Second, it enables financial institutions to collect customer data at scale and improve their offerings based on gathered insights. Third, mobile banking apps reduce reliance on physical branches, which means fewer customer-staff interactions and lower operational costs. We could continue like this for a long time, but rather than talk about theoretical benefits of mobile banking, let’s see it in action.

CRDB Bank case

CRDB Bank is the largest commercial bank in Tanzania, holding a 25% share of the country’s total banking assets. In 2011, it launched SimBanking—Tanzania’s first-ever mobile banking app. In 2022, the bank introduced a self-account onboarding feature in the app, allowing consumers to open accounts without visiting a branch. This feature alone brought in 68% of new customers that year, pushing the bank’s customer base to over 4 million users. A little later, the bank overhauled its application, digitizing 70% of banking processes and empowering customers with self-service options, which reduced branch reliance. This not only transformed customer experience in banking but also contributed to a rise in digital financial inclusion—from 65% in 2017 to 76% by 2023.

In summary, CRDB Bank’s mobile application helped the bank:

- Attract new customers through self-account onboarding.

- Digitize 70% of banking processes.

- Increase digital financial inclusion by 11 points.

- Expand the customer base to over 4 million people.

#2 AI brain, human heart

Over the years, we’ve seen the increasing adoption of AI in the banking industry. In 2023 alone, the financial services sector invested an estimated $35 billion in AI, with banking accounting for about $21 billion. Such huge investments shouldn’t be surprising, given how much artificial intelligence contributes to the banking service quality. It detects fraud faster and better than any human, it helps with customer support inquiries by answering FAQs in seconds, it personalizes the digital banking experience for each user by analyzing their preferences and behavioral patterns, and it automates data entry and other tasks, helping banks save millions of dollars.

However, you can’t rely on AI alone to improve banking customer experience. If anything, it can do more harm than good. Picture this: You open your banking app and notice an unfamiliar transaction that you’re 100% sure you didn’t make. You reach out to a customer support agent to resolve the issue, which happens to be an AI agent. The agent is unable to help, as, although it can see the transaction details, it takes a human to determine if the transaction was fraudulent or a mistake and take appropriate action. Yet, the AI doesn’t offer any clear way to connect with a human employee.

You might say that this example is exaggerated, but the issue is more common than you think. According to the RAND Corporation’s research, a staggering 80% of AI projects in banking don’t deliver on their promises. Another study by the Consumer Financial Protection Bureau revealed that many AI chatbots use limited rule-based systems and can trap customers in never-ending loops of repetitive responses, failing to offer any meaningful help.

“When consumers require assistance from their financial institution, the circumstances could be dire and urgent. Instead of finding help, consumers can face repetitive loops of unhelpful jargon. Consumers also can struggle to get the response they need, including an inability to access a human customer service representative. Overall, their chatbot interactions can diminish their confidence and trust in their financial institutions.”

The bottom line? Good customer service in banking still requires human touch, however enticing it might be to automate everything. Banks that implement AI should always remember that while their operations may run on an AI brain, they must maintain a human heart, especially when it comes to customer-facing areas like support. Sure thing, there is nothing wrong with using AI for easy-to-handle requests and frequently asked questions. In fact, some customers will be thankful for that, as AI agents reply in seconds and can resolve issues faster. However, it is crucial to allow consumers to be able to connect to a human agent if their issue is more complex—preferably, with something as simple as clicking a button.

One of the good examples of excellent customer service in banking with the help of AI is Singapore’s DBS Bank. The organization adopted a comprehensive AI strategy to support customer service, resulting in a 33% reduction in processing time for customer queries and being recognized as “World’s Best Digital Bank” by Euromoney. While AI handles routine requests, human agents step in for sensitive and intricate situations, making sure each issue is resolved to the customer’s utmost satisfaction.

#3 Banking that knows you

One of the most prominent customer experience trends in banking is personalization. According to Deloitte, more than 50% of bank customers believe personalized services are one of the key factors for them to have trust in their banks. What’s more, research by McKinsey shows that financial institutions that invest in personalizing their services generate 40% more revenue. Banks realize this potential and keep investing in data analytics, machine learning models, and AI technology to build systems that understand their customers and can offer relevant products and services at appropriate times.

Here are a few banks that are raising the bar in digital banking customer experience through smart personalization.

Bank of America

Bank of America launched Erica, a virtual financial assistant, in 2018. Since then, it has had over 2 billion interactions with its users, helping them manage their finances with ease. Powered by AI, Erica is highly versatile and can help bank customers with different requests while keeping their personal wants and needs in mind. For example, it’s used for monitoring and managing recurring subscriptions (2.6 million requests per month), helping clients understand their spending behaviors (2.2 million requests per month), keeping users informed about deposits and refunds (2.1 million requests per month), and much more. Erica can even send you a wish on your birthday or crack a joke when you need it.

ING Bank

To improve customer experience and boost client satisfaction, ING Bank developed an AI-powered recommendation engine that adds a personal touch that many bank clients of today expect. This solution analyzes transaction histories, browsing behaviors, previous interactions with the bank, and other customer data to tailor banking offers to each individual client. ING Bank’s search engine has delivered a positive impact across the customer journey. It has not only increased customer engagement and satisfaction but also cut costs on manual customer segmentation and campaign management.

Commonwealth Bank of Australia

Commonwealth Bank of Australia (or Commbank) understands the importance of quality customer service in banks and takes personalization to the next level through AI. The institution developed the Customer Engagement Engine (CEE), an AI-driven personalization platform that makes a staggering 55 million decisions daily, tailoring customer experiences across the mobile app, online banking, call centers, and ATMs. This engine uses data analysis and generative AI to unlock hyper-personalization capabilities. It made it possible for Commbank to design the “Benefits finder”—a tool that proactively notifies customers of government grants and rebates they are eligible for. This feature alone has successfully connected CBA customers with over $1 billion in payments, putting an average of $710 back into users’ pockets.

#4 Self-service when you want it, in-person support when you need it

It might seem that today bank branches are obsolete. The total number of active US bank branches has dropped below 65,000 this year, and over 8000 branches worldwide are projected to shut down. After all, we have over 300 neobanks that provide their services only through the internet and many more digital-first organizations, including modern startup banking platforms, offering a diverse range of self-service options. From opening a bank account to getting a car loan, the vast majority of banking operations can be done online. Just a few taps on your phone and you receive exactly what you need. So why bother going to a branch?

Well, while the said above rings true and branch foot traffic is indeed declining, many customers still rely on branches. According to a J.D. Power report, 72% of customers in 2023 expressed their intention to visit their banking branches as often as the previous year, while 38% said branches were essential. Older adults (65+) remain the most branch-reliant group, with 16% baby boomers visiting branches regularly. But even when it comes to Gen Zers, 65% prefer opening a bank account in person.

This begs the question: If digital banking is so prevalent and physical branches go out of fashion, why do they still matter? There are at least two explanations for this:

- Not every organization provides adequate self-service. In fact, 64% of consumers say their banking apps don’t allow them to solve their problems quickly, if at all.

- Some self-service options work best for banking-savvy consumers. Take personal loans, for example. They can be tricky and require a certain degree of knowledge from the borrower (especially when it comes to paying them back). Talking to a bank employee in person before applying for a loan can really help.

The most challenging aspect for a bank is to strike the right balance between self-service and in-person options. Self-service is often cheaper and easier to scale, but in-person support still matters to customers and is indispensable for complex banking products like personal loans. On the one side, there are consumers who prefer to act independently and don’t want to be forced into a branch for something as trivial as updating personal information. On the other side, there are clients with complex issues who rely on in-person interactions. To satisfy both and deliver the best customer experience in financial services, a bank must find a way to balance the digital convenience with the opportunity to request human guidance when needed.

#5 Multiple channels, one experience

A strategically crafted omnichannel customer experience is one of the emerging banking contact center trends that separates a good bank from a great one. Organizations with omnichannel engagement strategies retain 89% of their customers on average. What’s more, 40% of consumers won’t do business with a bank if it doesn’t provide their preferred communication channel. Given this, it shouldn’t be surprising that financial institutions establish multiple points of contact with their customers.

Modern banks can be reached through mobile apps, online banking platforms, email, chatbots, and, quite often, social media. However, omnichannel CX in banking is not about how many channels an institution has, but rather how seamless a customer’s experience across these channels is. As pointed out in the introduction, over 62% of bank clients want smooth transitions between channels (from mobile and web to branch and vice versa). Therefore, to provide the best omnichannel experience, an organization needs to ensure its customers can switch from one touchpoint to another without having to repeat themselves.

Picture this: You start filling out a loan application form on your smartphone—maybe for a personal loan or even a quick option like payday loans. At some point, you are asked to upload a photo of your document, which is stored on your computer. You decide to switch to your PC and finish the form there. If your bank has a thought-out omnichannel strategy in place and foresaw situations like this, you will be able to finish your form without re-entering information. However, if the bank provided omnichannel communication options without taking time to coordinate them, you will have to start from scratch (which is, sadly, often the case).

To see a real-world example of how a seamless omnichannel strategy works in practice, let’s take a look at Citibank.

Citibank case

Citibank developed an integrated platform that connects its mobile app, online banking portal, and branch operations. It allows customers to initiate transactions on one channel and complete them on another without disruption. For example, a customer can start a loan application on the mobile app, track its progress online, and finalize it in person at a branch, all without re-entering information or explaining their needs repeatedly.

Thanks to this approach, Citibank’s clients experience consistent service regardless of how they interact with the bank. The bank, in turn, collects and consolidates customer data, gaining a deeper understanding of client preferences and behaviors.

Wrapping Up

These were the top 5 consumer banking trends that can help you understand how to improve customer experience in banking and deliver exactly what your clients need. Let us summarize the key points:

- Implement a mobile-first approach to let users carry out banking operations without in-branch visits.

- Use AI smartly and don’t forget about the human touch during customer support and other customer-facing activities. Human interactions are still important in 2025 and will likely be that way for years to come.

- Use personalization. It’s a win-win strategy for both your organization and your customers: You increase revenue, your clients get offers tailored to their needs.

- Find a balance between self-service and in-person support. While self-service options are convenient for many, there are still people who rely on in-person assistance when dealing with banking products.

- Offer a seamless omnichannel experience. Make sure you not only provide different options to connect with your bank but also enable a smooth transition between channels so that your clients don’t have to repeat themselves or re-enter information.

Of course, it is easier said than done. Improving customer experience in financial services involves dealing with strict regulations, legacy systems, ever-changing client expectations, and a multitude of other challenges. Luckily, you don’t have to wade through them alone. If you need assistance with your customer experience initiatives, you can always count on Helpware CX!

Helpware CX is a team of professionals across 11 countries who speak 49+ languages and specialize in everything CX! From CX consulting to providing dedicated customer support—we will help you with anything you need and make customer experience your strongest competitive advantage. Drop us a line and tell us about your plans—we’ll get back to you within one business day.